Are digital bank facilities and online bank accounts any better or different from those of traditional banks?

Banking is an essential aspect of our daily lives, and with technology advancing every day, we now have more options than ever before.

Traditional banking has been around for centuries, while digital banks are a more recent development.

Both options have advantages and disadvantages, and deciding which is right for you can be challenging.

If you’re torn between choosing a traditional bank account or going digital, this article will compare the two options and help you make an informed decision.

From the security and convenience of digital banks to the personalised service and familiarity of traditional banking, we’ll compare each to help you find the best option for your financial needs.

By the end of this post, you’ll better understand which banking option is right for you.

Let’s get started!

What Is Traditional Banking?

Traditional banking refers to the conventional brick-and-mortar banking experience, where you can visit to open accounts, deposit or withdraw money, apply for loans, seek assistance from bank staff, and access other banking services.

They also provide in-person customer service and have a physical presence in the form of bank branches and ATMs.

Traditional banks typically have a wide range of products and services, including savings accounts, current accounts, credit cards, investments, personal loans, etc.

This method offers a personal touch, with face-to-face interactions and a sense of security, as customers can physically handle their money and documents.

Advantages of Traditional Banks

Physical Presence: One of the main benefits of traditional banks is that they have physical branches where customers can go and conduct their banking transactions. This provides security and convenience for customers who prefer face-to-face interactions when dealing with their finances.

Wide Range of Services: Traditional banks offer a wide range of services, including current and savings accounts, loans, credit cards, and investment options. This allows customers to meet all their financial needs in one place, making it easier to manage their money.

Established Reputation: These brick-and-mortar banks have been around for a long time and have established a reputation for being reliable and trustworthy. This gives customers a sense of trust and reliability, knowing that an established institution is handling their money.

Safety & Security: Traditional banks are regulated and insured, offering a level of security for customers’ deposits and transactions. Knowing that their funds are secured and protected can offer peace of mind.

Relationship Building: These banks often prioritise building long-term relationships with their customers, which can, in turn, lead to personalised financial advice, tailored product recommendations, and potential access to exclusive offers or benefits.

Cash Handling: Traditional banks have physical branches and ATMs where customers can deposit and withdraw cash. This can be advantageous for individuals who frequently deal with cash transactions or prefer the convenience of physical currency.

Disadvantages of Traditional Banks

Limited Accessibility: Unlike the digital bank, traditional banks have limited accessibility. Customers can only conduct their banking transactions during business hours, which may not be convenient for those with busy schedules.

Fees: Traditional banking often requires additional fees for services. These can include monthly maintenance fees, ATM fees, overdraft fees, and more. These fees can add up and significantly impact a customer’s finances, especially those with lower incomes.

Slow Processing Times: Transactions and processes in traditional banks can take longer than in online or digital banks. This includes check clearance, loan approvals, and account updates. This can be a disadvantage for individuals who require quick and efficient banking services.

Lower Interest Rates: Traditional banks often offer lower interest rates on savings accounts and other financial products compared to digital banks.

This means that customers may not earn as much interest on their money, which can be a disadvantage for those looking to grow their savings.

Lack of Innovation: These banks may be slower to adopt new technologies and innovations compared to online or digital banks. This can limit the availability of advanced features and services, such as mobile banking apps and digital payment options.

Paperwork and Documentation: With traditional banks, you might be required to go through extensive paperwork and documentation for various transactions, such as opening an account, applying for a loan, or making certain financial transactions.

What Is Digital Banking?

Digital banking, also known as Internet banking or online banking, refers to the electronic platform provided by banks and financial institutions that allows customers to perform various banking transactions and access financial services through the Internet.

It enables customers to manage their bank accounts, conduct financial transactions, and access banking services from the convenience of their computer, smartphone, or other internet-enabled devices.

With online banking, customers can manage their finances from the comfort of their own homes or on-the-go.

It allows users to perform various banking activities, including checking account balances, transferring funds, paying bills, and even applying for loans, all through secure online platforms.

Advantages of Digital Banks

Easy Accessibility: With just a few clicks, you can access your account 24/7, make transactions, check balances, and pay bills from the comfort of your own home or anywhere with an internet connection.

This convenience is especially beneficial for individuals with busy schedules or limited mobility, as it eliminates the need to visit a physical branch.

Lower Fees: In many cases, account fees at online banks are lower than they are at traditional banks.

For instance, most digital banks don’t charge a monthly account maintenance fee, whereas many traditional banks do. This can result in lower fees and higher interest rates on savings accounts.

Enhanced Security: Online banking platforms usually employ advanced security measures, such as encryption and multi-factor authentication, to protect your account and personal information. Additionally, online banking reduces the risk of physical theft or loss of sensitive documents.

Paperless Transactions: Online banking promotes environmental sustainability by reducing the need for paper statements, checks, and other physical documents, which can contribute to a more eco-friendly banking experience.

Quick and Efficient Transactions: This Internet banking system allows for faster processing of transactions compared to traditional banking methods.

Transfers between accounts, bill payments, and other transactions can be completed with just a few clicks, saving time and effort.

Faster Access to Financial Information: With online banking, you can quickly access real-time information about your account balances, transaction history, and pending transactions.

This provides you with up-to-date financial information, allowing for better financial planning and decision-making.

Disadvantages of Digital Banks

Limited Physical Presence: Online banks do not have physical branches, so you may not have access to in-person customer service or assistance. This can be a disadvantage for individuals who prefer face-to-face interactions or need immediate support.

Dependence on Technology: Online banking requires access to internet-enabled devices, such as computers or smartphones. If you don’t have reliable internet access or encounter technical issues with your devices, it may hinder your ability to manage your account effectively.

Security Concerns: While online banking platforms have robust security measures, there is still a risk of online fraud, phishing attacks, or identity theft. It’s important to be vigilant, use strong passwords, and follow best security practices to mitigate these risks.

Limited Cash Access: Online banks may have limited options for depositing or withdrawing cash into your account. This can be a disadvantage for individuals who frequently deal with cash transactions or prefer the convenience of physical currency.

Potential for Technical Glitches: While online banking platforms strive to provide a smooth user experience, there is always a possibility of technical glitches or system failures. This can temporarily disrupt your access to your account or cause delays in processing transactions.

Learning Curve: Some individuals may need help adapting to the online banking interface or navigating the various features and functions. However, most online banking platforms are designed to be user-friendly and offer customer support to assist with any difficulties.

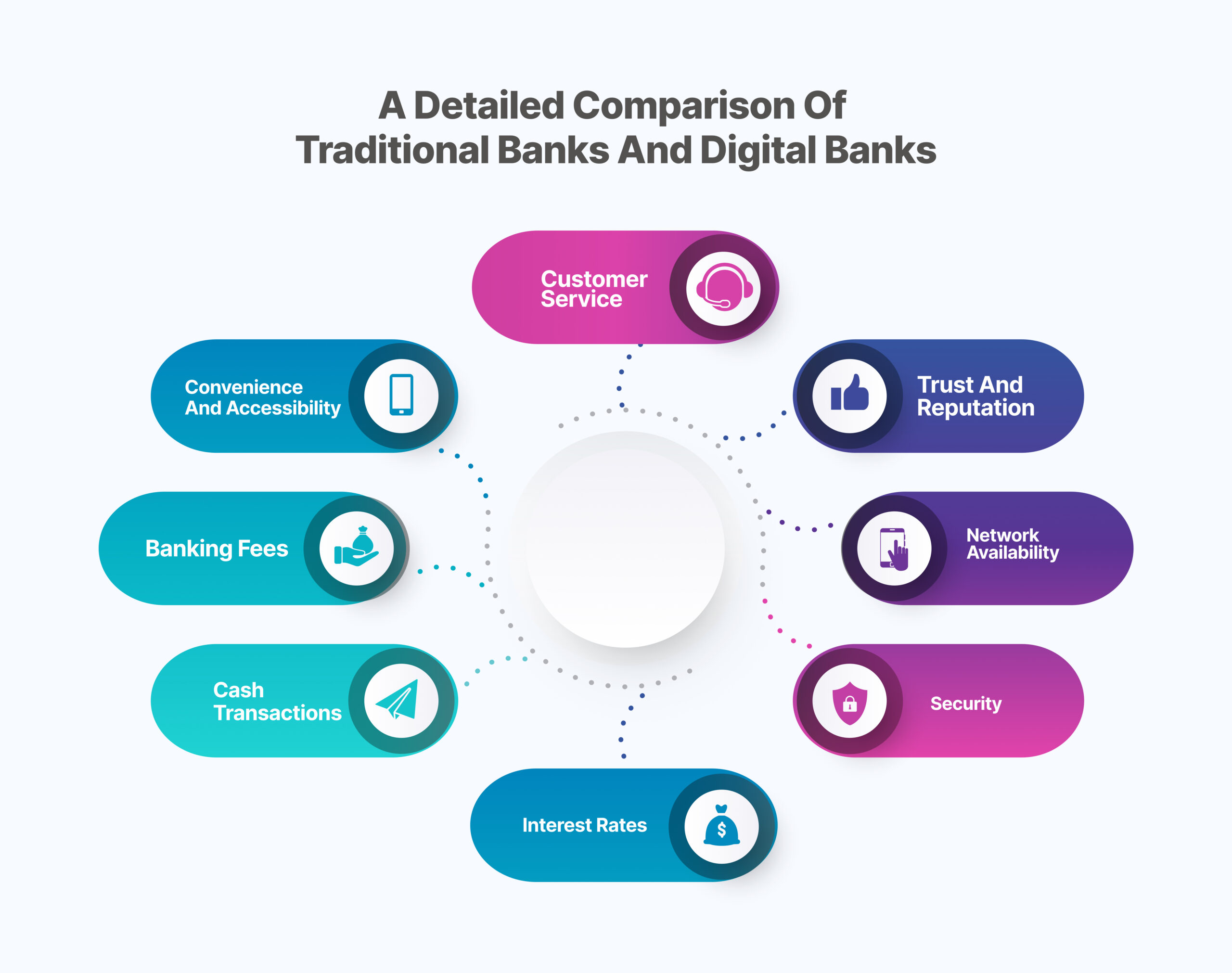

A Detailed Comparison of Traditional Banks and Digital Banks

In this section, we compare the differences between traditional banking and online banking, to help you make an informed decision.

Convenience and Accessibility

One of the main advantages of online banks is the convenience they offer. With online banks, customers can access their accounts and perform various banking transactions from the comfort of their own homes or on the go using their smartphones or computers.

Traditional banks, on the other hand, require customers to physically visit a branch during specified hours, which can be inconvenient for those with busy schedules.

Customer Service

Customer service is another crucial aspect to consider when comparing traditional banks and online banks. Traditional banks often have a physical presence and offer face-to-face interactions with bank representatives, which can benefit individuals who prefer personal assistance.

Online banks, however, provide customer service primarily through phone, email, and online chat, eliminating the need for in-person contact. Online banks are known for their prompt and efficient customer service, often available 24/7.

Banking Fees

Regarding fees, online banks have a clear advantage over traditional banks. Online banks typically have lower fees, as they have lower overhead costs compared to traditional banks.

This means that you can save money on monthly maintenance fees, ATM fees, and other charges by choosing an online bank.

Interest Rates

Online banks often offer higher rates on savings accounts and lower rates on loans when compared to traditional banks. This can be a significant advantage for individuals looking to maximise their savings or secure a loan at a lower cost.

Cash Transactions

Traditional banks allow customers to conduct cash transactions easily. Customers can deposit cash into their accounts by visiting a branch or using ATMs that accept cash deposits. They can also withdraw cash from ATMs or over the counter at branches.

In contrast, online banks may have limitations regarding cash transactions. Since they lack physical branches, depositing or withdrawing cash can be more challenging.

However, some online banks often partner with other financial institutions or use ATMs from partner networks to provide cash services to their customers.

Network Availability

Traditional banks have a widespread network of physical branches and ATMs, providing customers easy access to banking services.

Customers can easily visit branches or ATMs to deposit or withdraw cash, speak with bank representatives, and perform various transactions.

On the other hand, online banks operate solely through digital platforms, which means they rely on internet connectivity for customers to access their services.

While digital banks provide 24/7 access to banking services through mobile apps and websites, customers need a stable internet connection to perform transactions and access their accounts.

Security

Traditional and digital banks prioritise the security of their customers’ personal and financial information.

However, digital banks have advanced security measures in place, such as multi-factor authentication and encryption, to protect against online threats. Individuals must ensure they choose a reputable online bank with robust security protocols.

Trust and Reputation

Traditional banks have been around for a long time and have established a reputation based on their history, stability, and reliability.

Customers often feel a sense of trust and security when dealing with traditional banks because they have a track record of serving customers and managing their finances.

On the other hand, digital banks are relatively newer in the banking industry. They operate solely through digital platforms, without any physical branches.

This lack of physical presence can sometimes make customers sceptical about the legitimacy and security of Internet banking.

Bottom Line

Whether you go with a traditional or digital bank depends a lot on your banking needs, not to mention your preferences and budget.

While traditional banks provide face-to-face interactions and a personal touch, they may be less convenient due to limited operating hours and higher fees.

On the other hand, digital bank accounts offer convenience, flexibility, high-interest rates, and enhanced security measures.

Remember, no law says you can have only one account — you might prefer to keep your money at a traditional bank but use an online savings account for the great interest rates. It’s totally up to you.

Mintyn is one of the fastest-growing digital banks in Nigeria. Mintyn offers savings, current and business bank accounts. Other innovative and support features are also available to improve your banking experience. You should try Mintyn today.

We hope this article has provided valuable insights to help you make the right choice.

Feel free to share your thoughts or ask questions in the comments section.

Leave a Reply